All Categories

Featured

Table of Contents

[/image][=video]

[/video]

Assuming rates of interest remain strong, even greater guaranteed prices might be possible. It's an issue of what terms finest suit your financial investment demands. We tailor several techniques to maximize development, revenue, and returns. Making use of a laddering strategy, your annuity profile renews every pair of years to make best use of liquidity. This is a wise technique in today's increasing rate of interest price setting.

MYGA's are one of the most prominent and one of the most common. With multi-year accounts, the price is secured in for your chosen duration. Rates are assured by the insurance coverage firm and will neither enhance nor reduce over the picked term. We see passion in temporary annuities supplying 2, 3, and 5-year terms.

Jackson Annuity Rating

Which is best, straightforward interest or intensifying interest annuities? The response to that depends upon exactly how you use your account. If you don't plan on withdrawing your rate of interest, after that generally uses the highest possible rates. The majority of insurance provider just provide intensifying annuity policies. There are, nevertheless, a couple of plans that credit scores easy rate of interest.

It all depends upon the hidden price of the fixed annuity agreement, naturally. We can run the numbers and compare them for you. Allow us know your purposes with your interest earnings and we'll make appropriate suggestions. Experienced taken care of annuity investors know their premiums and rate of interest gains are 100% available at the end of their picked term.

Unlike CDs, repaired annuity policies allow you to withdraw your passion as income for as long as you desire. And annuities offer greater prices of return than nearly all comparable bank tools offered today.

There are several highly ranked insurance business competing for down payments. There are a number of popular and highly-rated business providing competitive yields. And there are agencies specializing in rating annuity insurance policy companies.

These qualities go up or down based on a number of variables. Insurance coverage business are generally risk-free and protected institutions. Very couple of ever before fail given that they are not permitted to lend your deposits like banks. There are several ranked at or near A+ supplying several of the best yields. A couple of that you will certainly see above are Dependence Standard Life, sis business Midland and North American Life, Americo, Oxford Life, American National, Royal Neighbors, Pacific Guardian Life, Athene, Sagicor, Global Atlantic, and Aspida among others.

They are safe and trusted policies developed for risk-averse capitalists. The investment they most very closely resemble is deposit slips (CDs) at the bank. View this short video to comprehend the similarities and differences between the two: Our customers buy taken care of annuities for several factors. Safety and security of principal and ensured interest prices are definitely two of one of the most essential elements.

Future Value Annuities Table

We aid those needing instant interest revenue now as well as those planning for future revenue. It's vital to keep in mind that if you require income now, annuities function best for those over age 59 1/2.

We are an independent annuity broker agent with over 25 years of experience. We assist our clients secure in the highest possible returns feasible with secure and safe and secure insurance policy business.

In recent times, a wave of retiring child boomers and high rates of interest have actually assisted fuel record-breaking sales in the annuity market. From 2022 to 2024, annuity sales topped $1.1 trillion, according to Limra, an international research company for the insurance coverage sector. In 2023 alone, annuity sales boosted 23 percent over the prior year.

Aged Annuity Leads

With more prospective rate of interest cuts imminent, uncomplicated fixed annuities which often tend to be much less difficult than various other choices on the market may come to be much less interesting customers as a result of their subsiding rates. In their location, other ranges, such as index-linked annuities, may see a bump as customers seek to catch market growth.

These rate walkings provided insurer space to provide more attractive terms on repaired and fixed-index annuities. "Passion rates on repaired annuities additionally rose, making them an appealing investment," says Hodgens. Also after the securities market rebounded, netting a 24 percent gain in 2023, remaining worries of a recession kept annuities in the limelight.

Other factors likewise added to the annuity sales boom, including even more banks currently offering the products, states Sheryl J. Moore, Chief Executive Officer of Wink Inc., an insurance coverage marketing research firm. "Customers are hearing concerning annuities more than they would certainly've in the past," she states. It's also much easier to acquire an annuity than it utilized to be.

"Literally, you can make an application for an annuity with your representative through an iPad and the annuity is accepted after completing an on the internet kind," Moore claims. "It utilized to take weeks to get an annuity through the concern procedure." Set annuities have driven the current development in the annuity market, representing over 40 percent of sales in 2023.

But Limra is expecting a pull back in the popularity of fixed annuities in 2025. Sales of fixed-rate deferred annuities are expected to go down 15 percent to 25 percent as rates of interest decrease. Still, dealt with annuities have not lost their glimmer quite yet and are using conservative investors an eye-catching return of even more than 5 percent in the meantime.

Reversionary Annuities

Variable annuities often come with a washing checklist of charges death expenditures, management expenses and financial investment management costs, to name a few. Fixed annuities keep it lean, making them an easier, less costly choice.

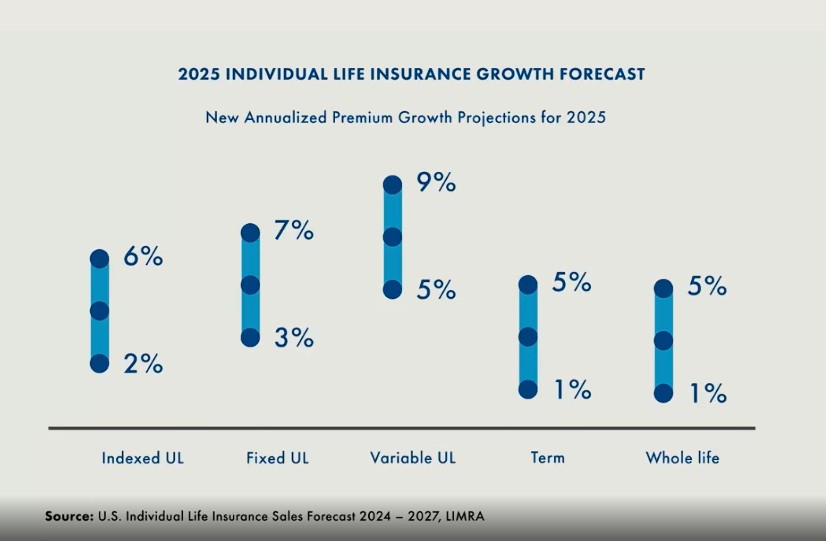

Annuities are complex and a bit various from other monetary items. (FIAs) damaged sales records for the third year in a row in 2024. Sales have almost doubled because 2021, according to Limra.

Nevertheless, caps can differ based on the insurer, and aren't likely to remain high forever. "As rates of interest have been coming down lately and are expected to find down additionally in 2025, we would expect the cap or engagement rates to also come down," Hodgens says. Hodgens expects FIAs will certainly stay appealing in 2025, yet if you're in the marketplace for a fixed-index annuity, there are a few points to look out for.

So in theory, these hybrid indices aim to ravel the highs and lows of an unstable market, yet actually, they have actually commonly dropped brief for customers. "A lot of these indices have returned little to absolutely nothing over the previous number of years," Moore claims. That's a challenging tablet to ingest, taking into consideration the S&P 500 published gains of 24 percent in 2023 and 23 percent in 2024.

The more you research and search, the more probable you are to locate a trustworthy insurer willing to provide you a suitable rate. Variable annuities once controlled the market, but that's altered in a huge way. These items suffered their worst sales on document in 2023, dropping 17 percent contrasted to 2022, according to Limra.

Mortgage Annuity

Unlike repaired annuities, which use downside defense, or FIAs, which balance security with some development possibility, variable annuities supply little to no protection from market loss unless motorcyclists are added on at an included expense. For financiers whose top concern is preserving capital, variable annuities merely don't determine up. These products are likewise infamously complex with a background of high costs and large abandonment fees.

When the market collapsed, these riders ended up being responsibilities for insurance companies due to the fact that their guaranteed worths exceeded the annuity account worths. "So insurance provider repriced their cyclists to have much less appealing functions for a higher price," claims Moore. While the market has actually made some efforts to enhance transparency and decrease costs, the item's past has actually soured numerous customers and monetary consultants, who still check out variable annuities with uncertainty.

Ing Usa Annuity And Life Insurance

RILAs provide customers a lot higher caps than fixed-index annuities. Just how can insurance coverage business pay for to do this? Insurance companies make money in various other means off RILAs, generally by paying investors much less than what they earn on their investments, according to an evaluation by the SEC. While RILAs seem like a good deal what's not to love about higher prospective returns with less charges? it is very important to understand what you're enrolling in if you remain in the market this year.

For instance, the large range of crediting methods used by RILAs can make it difficult to compare one product to an additional. Higher caps on returns also include a trade-off: You tackle some risk of loss past a set flooring or buffer. This barrier shields your account from the initial section of losses, typically 10 to 20 percent, however afterwards, you'll lose money.

{kind=link}

Table of Contents

Latest Posts

Global Atlantic Annuity Phone Number

Annuity Laddering

Allianz 222 Annuity

More

Latest Posts

Global Atlantic Annuity Phone Number

Annuity Laddering

Allianz 222 Annuity